Only three companies in the world make the heat-resistant blades that spin inside a power-plant turbine. They're sold out through 2030. This is what's holding up the AI buildout.

By 2030, data centers will draw about as much electricity as Japan does today. In the U.S. alone, they'll out-burn aluminum, steel, cement, and chemical production combined.

So where does the marginal kilowatt come from?

Mostly natural gas. Which means more gas plants, which means more turbines, and turbines now have a 5 to 7 year wait list. Siemens has its biggest backlog ever. Mitsubishi is sold through 2028. Even with all three majors expanding, total industry output goes up maybe 25%. Some hyperscalers are bolting cruise-ship and warship turbines to semi-trucks because that's faster than buying a real one.

When the bottleneck is "we can't make turbine blades fast enough," it's worth asking what doesn't need turbines.

The most aggressive answer comes from SpaceX. In January, they filed for a constellation of up to a million data center satellites in orbit, solar-powered, and merged with xAI to actually build it. Musk says space will be the cheapest place to put AI within 36 months. The proposal sounds insane. Then you run the numbers.

So let's run them.

Solar avoids the turbine problem

Solar farms have no turbines, no fuel chain, no cooling water, no boiler. Permit to power: about 18 months. Panels are commodity hardware, China makes them at 10 cents a watt, and they could ship more tomorrow.

So why isn't solar covering Nevada?

Two reasons.

The first is permits. Try fencing off a few hundred square miles of public desert and watch what happens.

The second is physics. Above the atmosphere, sunlight hits every square meter at full strength, all day, all year. Drop into the atmosphere and clouds, scattering, night, and angle eat about 80% of it. The same panel on Earth gets about a fifth of what it would get in space.

That's the punchline: same panel, 5x more energy per year in orbit.

You also stop needing batteries. A satellite in high orbit sees the sun nearly 24/7, eclipsed only briefly twice a year. Earth solar farms need 4 to 8 hours of storage to act as baseload, which roughly doubles the project cost.

The mass problem

Lifting kilograms is expensive, so the real question becomes: how heavy is a panel?

A rooftop panel is mostly tempered glass and an aluminum frame, both there to survive hail and wind. The actual cell is a thin slice. The whole module weighs about as much as five large textbooks per square meter.

A space panel doesn't need glass. No hail, no wind, no rain. You can use plastic film as the substrate. Today's space-grade flexible panels are about a third of a rooftop panel. Caltech's prototypes, already flown, weigh 300 times less than rooftop. They beamed power down from orbit in 2023.

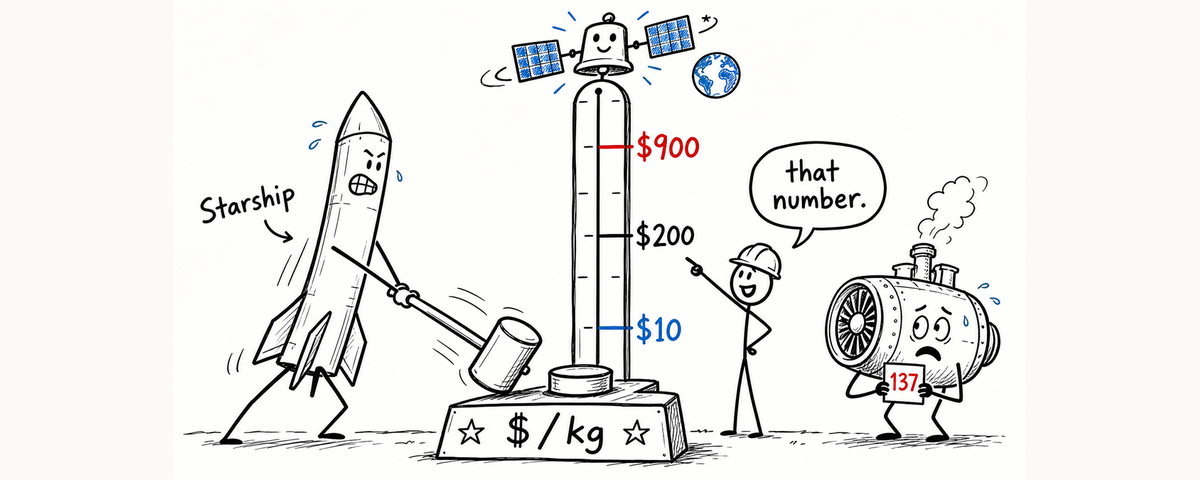

Now the launch cost. Falcon 9 runs about $2,500 per kilogram. Starship today is around $900. SpaceX's near-term target is $200. The stretch goal is $10.

For a 1 GW orbital array (one major AI data center, roughly a million homes), the launch math comes out like this:

- Today's panels at today's Starship: about $7B in launch alone.

- Today's panels at $200/kg: about $1.5B.

- Caltech panels at $200/kg: about $25M.

That's launch only. Panels, structure, chips, and assembly add billions on top, and the proper apples-to-apples comes later. But launch is the variable that scales. As $/kg drops, every other piece of the orbital stack gets cheaper too.

Cable, beam, or move the data center

How does the power get back to Earth?

It can't. No material can hang under its own weight from 36,000 kilometers. From low orbit, satellites move 8 km/s relative to the ground, so a tether is out too.

Microwaves work, but you lose about half the power round trip and the receiving antenna ends up 1 to 10 kilometers wide.

So SpaceX's plan is option three: don't bring the power down, move the data center up. Put GPUs next to the panels, beam the answers home. AI responses are tiny compared to the energy needed to compute them. No transmission loss. No giant antenna farm in the desert.

What actually limits this

The orbital pitch has four real bottlenecks. They stack roughly in this order of severity.

1. Cooling

Nobody talks about this one. A data center turns essentially all its electricity into heat. On Earth, you blow air over it or pump water through it. In space, neither works. No air, no water. The only way out is to radiate the heat into the cold of space.

Sounds easy because space is cold. It isn't, because radiation is slow. Dumping 1 GW of waste heat needs 1 to 2 square kilometers of radiator surface, comparable to the solar array itself. The ISS rejects 70 kilowatts with about 1,000 m² of radiator. A centralized 1 GW system in orbit would dwarf anything ever flown.

The fix is to not centralize. SpaceX's plan is a constellation of 1 MW satellites, and at that scale each radiator is about 1,200 m², comparable to large deployable structures already flying today. Starcloud, Axiom Space, and Sophia Space are testing megawatt-class thermal designs in orbit right now. Distributing the compute dissolves the centralized cooling problem by refusing to concentrate it.

The cost still adds up. Cooling roughly doubles launch payload per gigawatt, another $2B at the $200/kg launch price. But it's a tractable engineering problem at the per-satellite level, not the wall it's sometimes painted as.

2. Launch cost

The cheaper a kilogram is to launch, the better orbital looks.

- Today (~$900/kg): orbital is 2 to 3 times more expensive than terrestrial.

- At $200/kg: roughly even, with lighter panels tipping it.

- At $50/kg: clearly cheaper than Earth.

- At $10/kg: the discussion ends. Orbital wins by 10x.

Whether $200 is reachable depends on Starship reuse, how many flights each booster can survive. That's the single most important number in the entire pitch.

3. Radiation (smaller problem than expected)

In space, energetic particles from the sun and from deeper in the galaxy hit chips constantly. They flip bits and can cause errors. The standard intuition was that modern AI chips, with their tiny transistors, would be especially vulnerable, and the standard story treated radiation as a major obstacle to orbital compute.

The actual data has come back better than expected.

Google ran its Trillium TPU through a proton beam in late 2025 and saw no hard failures at twenty times the expected five-year mission dose. Memory was the most sensitive component, and even it stayed reliable through three times mission lifetime. With reasonable shielding, modern AI chips can survive multi-year orbital missions without permanent damage.

What's left is bit flips, soft errors that need error correction to handle. The overhead is modest, and terrestrial data centers already do something similar. Five years ago the picture was that orbital compute would need chips a decade behind cutting edge. Today's picture: the latest commercial accelerators work fine in space.

This was supposed to be a major bottleneck. It's turning out to be a minor one.

4. China

About 80% of the world's solar panels, and most of the upstream materials, come from China. The U.S. and Europe combined make under 10%. Putting solar in orbit doesn't change any of that. You still need cells, and the orbital pitch increases panel demand, not decreases it.

Three options: accept the dependency, pay 2 to 3 times more for U.S. or European cells, or wait 5 to 10 years for new capacity to come online.

This is the bottleneck without a Starship to fix it.

What it would take

Most of the apparent challenges turn out to be one challenge in disguise.

Cooling, panel weight, structural mass: they're all mass problems. And mass is just launch cost. If a kilogram is cheap enough to launch, you stop optimizing for it. Use heavy radiators. Use today's space-grade panels instead of Caltech prototypes. Use commercial chips with shielding. The brute-force version works as long as the launch math works.

Apples-to-apples numbers. A 1 GW orbital data center built with today's heavier components weighs about 26,000 tons. At $200 per kilogram, launch alone is about $5B, and once you add panels, radiators, satellite buses, and chips, the all-in runs around $28-30B (per a 2025 Natixis analysis). Compare that to a terrestrial 1 GW AI campus, which Bernstein puts at around $35B all-in. Same ballpark. At $50/kg, the orbital total drops to about $25B, clearly cheaper than Earth. At $10/kg, launch is essentially free, and orbital wins comfortably.

So the real question is whether launch gets cheap enough. That requires Starship to fly at airline-like cadence: each booster reused dozens of times, the factory shipping rockets weekly instead of monthly. SpaceX did the smaller version of this with Falcon 9. Whether they pull it off again with a vehicle ten times the size is the entire bet.

One thing doesn't dissolve with cheap launch.

China still makes the panels. About 80% of global solar manufacturing. Cheap launch just means buying more Chinese panels. Building alternative capacity at scale is a political question, comparable to a CHIPS Act for solar, not an engineering one.

Everything else is downstream of one number: dollars per kilogram to orbit.

What it adds up to

A panel in orbit runs at roughly five times the energy density of a panel on the ground: no batteries, no hail, no glass. A turbine rotor doesn't run at all. It's gated by three foundries and a decade of forging capacity that doesn't exist.

The orbital version wins or loses on one number: dollars per kilogram to orbit. Below $200, it wins. Above, it doesn't. Cooling area, panel weight, chip shielding: all downstream of that one variable.

A long rocket and a thin panel might just be cheaper and faster than waiting in line for a turbine.

Notes on the math

For readers who want to dig into the numbers, because you should never "just trust me bro".

Demand projection. Global data center electricity consumption was 415 TWh in 2024, projected to 945 TWh by 2030, per the IEA's Energy and AI report (April 2025). One TWh is a billion kWh. Goldman Sachs Research separately projects a 160-165% increase in data center power demand over the same period. By 2030, U.S. data centers will consume more electricity than all U.S. heavy industry combined.

Turbine bottleneck. Lead times for new combined-cycle gas turbines now run 5-7 years. Siemens Energy backlog: €136 billion. Mitsubishi Power sold out into 2028. The three majors (GE Vernova, Siemens Energy, Mitsubishi Power) hold ~75% of global market share. Industry-wide expansion plans imply 20-25% output growth against demand growing roughly 3x faster. Grid interconnection in major U.S. data center markets now takes 36-84 months.

The 5x ratio. The solar constant, the sun's energy hitting any flat surface above the atmosphere, is 1,361 W/m², continuous. Average insolation at Earth's surface, integrated across a year (including night, weather, latitude, and seasonal variation): roughly 200-250 W/m². Ratio: 1,361 ÷ 250 ≈ 5.4.

Panel weight. A standard rooftop silicon module weighs about 10-12 kg/m² and outputs ~200 W/m² peak, about 20 W/kg. Current space-grade flexible arrays (e.g., the Roll-Out Solar Array on the ISS) hit about 150 W/kg. Caltech's Space Solar Power Project has demonstrated panels targeting 6.6 kW/kg, at 0.05 kg/m², using 25-30% efficient multijunction cells.

Mass for 1 GW continuous, in orbit. With 30% efficient cells receiving the full solar constant, output is ~408 W/m². For 1 GW continuous: 2.45 million m² of panel needed.

- At 3 kg/m² (today's space-grade flexible): 7,400 tons

- At 1 kg/m² (mid-term realistic): 2,500 tons

- At 0.05 kg/m² (Caltech target): 125 tons

Mass for 1 GW continuous, on Earth. At a typical 25% capacity factor, you need 4 GW of nameplate capacity. At 200 W/m² module output: 20 million m² of panel. At 10 kg/m²: ~200,000 tons of glass and aluminum.

Launch cost. Falcon 9 today: ~$2,500/kg to LEO. Starship list price (per Voyager Technologies' SEC filing for a 2029 launch): $90M for ~100 tons → ~$900/kg. SpaceX target as Starship matures: $100-200/kg. Musk's stretch goal: $10/kg.

Cooling math. A radiator surface at 70°C (343 K) radiates roughly 700 W/m² at the theoretical maximum, by Stefan-Boltzmann: P/A = ε × σ × T⁴, with emissivity ε ≈ 0.9. After accounting for solar absorption and Earth IR pickup in LEO, real-world net rejection is closer to 500 W/m² for a well-designed two-phase pumped loop. For 1 GW of heat: ~2 million m² of radiator. At 5-10 kg/m² for radiator panels with heat pipes and fluid loops: 10,000-20,000 tons of additional payload.

ISS reference and distributed architecture. The ISS's External Active Thermal Control System uses ~1,000 m² of radiator to reject ~70 kW. A single, centralized 1 GW orbital data center radiator would be a 14,000x scale-up by power capacity (or ~2,400-5,000x by surface area). However, SpaceX's actual proposal is a distributed constellation of much smaller satellites, each handling roughly 1 MW of compute. At that per-satellite scale, each radiator is on the order of 1,200 m², comparable to large deployable structures already flying (e.g., AST Mobile's 20×20m phased array antenna). Several startups are testing megawatt-class thermal designs in orbit: Starcloud (passive radiative cooling on its first H100 satellite, launched November 2025; planning a "Hypercluster" by October 2026), Axiom Space (thermal tiles developed with Spacebilt, launched January 2026), and Sophia Space (modular tile architecture integrating solar cells and radiators on opposite faces).

Microwave power transmission. Beaming uses 2.45 or 5.8 GHz frequencies, with a rectifying antenna ("rectenna") on the ground to convert microwaves back to electricity. Caltech's MAPLE experiment (March 2023) demonstrated wireless power transfer from LEO. End-to-end efficiency including all conversion and atmospheric losses runs 50-60%. Receiver diameter for 1 GW received: 1-10 km depending on frequency and orbit altitude.

Radiation. The intuition that modern AI chips would be especially vulnerable to space radiation has not held up in actual testing. Google's Project Suncatcher team tested its Trillium TPU (Google's v6e Cloud TPU) in a 67 MeV proton beam in late 2025. Annual shielded radiation dose in LEO: ~150 rad(Si)/year, or ~750 rad(Si) over a five-year mission. The high-bandwidth memory subsystem (the most sensitive component) only began showing irregularities at 2 krad, about 3x the five-year mission dose. No hard failures attributable to total ionizing dose were observed at the maximum tested level of 15 krad, about 20x the five-year mission dose. Google describes this as "remarkable radiation resistance for space applications." Soft errors (bit flips) still occur and require error-correcting code memory and selective redundancy in critical paths, but standard ECC overhead is on the order of 10-15%, not the 30% sometimes cited for full triple-modular redundancy. With reasonable shielding, modern commercial AI chips can survive multi-year LEO missions without permanent damage.

China supply chain. China's share of global solar manufacturing: ~80% of polysilicon, ~95% of wafers, ~80% of cells, ~75% of finished modules (varies year to year). U.S. and European combined manufacturing share: under 10%.

Cost comparison. Natixis modeled a 1 GW orbital data center system at $28-30 billion total capital cost, assuming $200/kg launch and lightweight panel and radiator designs. For terrestrial 1 GW AI data centers, estimates vary by source: Bernstein (October 2025) puts the all-in cost at around $35 billion; Nvidia has cited $50-60 billion for future GPU cycles; industry consensus on a current GB200-class 1 GW deployment is roughly $30-50 billion all-in (chips, facility, cooling, power supply). At $200/kg launch, orbital and terrestrial are in the same ballpark. Below that price point, orbital becomes increasingly cheaper.

Starship economics for the $200/kg target. A Starship vehicle costs ~$90M to construct. To reach $10-100/kg launch costs, the vehicle has to fly approximately 100 times to spread that construction cost across enough missions. Falcon 9 has demonstrated 25+ flights per booster; one booster crossed 30. SpaceX flew 5 Starship test flights in 2025 against a stated target of 25, a 5x miss. The FAA has authorized up to ~145 Starship launches per year across all SpaceX pads (Starbase + LC-39A + SLC-37) by 2027. Starship V3, debuting in 2026, is rated for 100+ tons to LEO in fully reusable configuration, ~3x the V2 capacity.

Why radiation hardening is less critical than once thought. Historically, satellites have used dedicated radiation-hardened processors built on much older fabrication nodes (the most advanced rad-hard processor in production, BAE Systems' RAD510, is on a 45-nanometer silicon-on-insulator process; modern AI accelerators are on 3-5 nanometer processes). The intuition was that closing this gap, five to ten generations of fab capability, would require new specialty fabs at multi-tens-of-billions cost. Google's Project Suncatcher findings on the Trillium TPU, published November 2025, suggest this gap may not need to be closed at all: commercial AI chips with reasonable composite shielding (e.g., Cosmic Shielding's "Plasteel," tested on the ISS during the Ax-2 mission) appear to survive multi-year LEO missions. The conclusion across industry is shifting from "we need rad-hard versions of frontier chips" to "commercial chips plus shielding plus error correction is enough."

Brute-force orbital scenario (heavy components, cheap launch). A 1 GW orbital data center built with today's components, space-grade flexible panels at 3 kg/m², heat-pipe radiators at ~7 kg/m², plus structure and chips, masses about 26,000 tons. The full all-in cost breakdown at $200/kg launch runs roughly: panels (commercial space-grade at scale) ~$5B, radiators ~$2-4B, chips ~$10-15B, structure and satellite buses ~$2B, launch ~$5B, total ~$25-30 billion. At $50/kg launch, the launch portion drops to ~$1.3B and the total falls to ~$22-26B. At $10/kg, the launch portion is ~$260M and the total is ~$20-23B. The launch component scales most aggressively as the rocket gets cheaper; the manufactured components stay roughly fixed at scale. Orbital is comparable to a $30-50B terrestrial 1 GW campus at $200/kg, clearly cheaper at $50/kg, and significantly cheaper at $10/kg.

Inference vs. training split. The dominant share of AI compute demand is and will increasingly be inference, not training. Deloitte estimates inference at ~67% of total AI compute in 2026, up from ~50% in 2025 and ~33% in 2023. McKinsey forecasts inference at ~50% larger than training by 2030 (93 GW vs 62 GW of global data center demand). Industry analysts estimate inference accounts for 80-90% of total lifetime compute cost of a deployed AI system. Most inference workloads (chat, batch processing, agentic workflows) tolerate the ~30-50ms latency of LEO data centers; only hard-real-time inference (autonomous vehicles, robotics, voice agents) requires sub-100ms total latency, which space cannot provide and which runs at the edge instead.

Written with ❤️ by a human (still)